Considering buying a house in 2025 instead of 2024? While it's natural to weigh your options, waiting out the market might not be the best strategy, especially if you're ready to take the plunge into homeownership.

The real estate market is dynamic and ever-changing, with speculation about the future often abound. However, there's no guarantee that waiting will yield a better deal or more favorable conditions. In many cases, delaying your home purchase will end up costing you more in the long run.

Interest rates are a key factor to consider. While historically low rates were prevalent for several years until they began to climb in mid-2022, they are now predicted to start decreasing again, increasing buyer purchasing power and competition. Waiting until 2025 might mean benefiting from lower interest rates, but it will undoubtedly bring more competition to an already low inventory market.

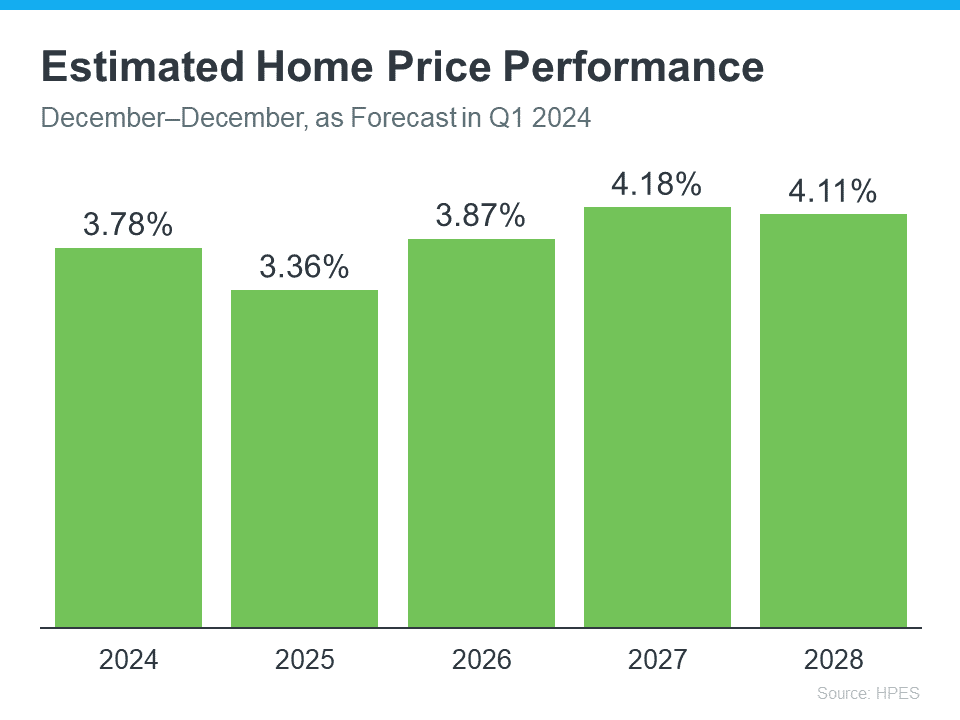

Every quarter, Fannie Mae and Pulsenomics release findings from the Home Price Expectations Survey (HPES), where over 100 experts, including economists, real estate professionals, investment analysts, and market strategists, share their insights on future home price trends.

In the latest survey, experts predict that home prices will continue to rise for the next five years. According to Keeping Current Matters, they expect a 3-4% rise each year, with no price declines anticipated. While home prices may not climb as much in 2025 as they are in 2024, these increases can accumulate over time, potentially resulting in higher costs for the same property if purchased later.

Home prices have been on the rise in many areas, and while future trends are uncertain, economists predict continued appreciation in 2025. By waiting, you could end up paying more for the same property than if you had bought it in 2024.

It's essential to consider the opportunity cost of waiting. Delaying your purchase means missing out on the benefits of homeownership, such as building equity, tax deductions, paying down principal, and personalizing your space.

Ultimately, the decision to buy in 2024 or wait until 2025 depends on your individual circumstances and financial situation. If you're financially ready and able to secure a mortgage with favorable terms, don't let uncertainty hold you back. The best time to buy is when you're ready, so if that time is now, seize the opportunity and make your move into homeownership.